![]() When Walmart exploded in the grocery industry in the 1990s and the first decade of the 21st century, eventually becoming the nation’s largest food retailer, the impact on the food retailing industry was significant. Food retailers, particularly supermarkets, had a powerful competitor and sought ways to compete. Not since the late 1940s and 1950s, when the modern-day supermarket became commonplace, had a single player impacted the grocery industry across the entire nation. The Food Institute has been following these types of trends and reporting on them to the entire found industry since its founding back in 1928.

When Walmart exploded in the grocery industry in the 1990s and the first decade of the 21st century, eventually becoming the nation’s largest food retailer, the impact on the food retailing industry was significant. Food retailers, particularly supermarkets, had a powerful competitor and sought ways to compete. Not since the late 1940s and 1950s, when the modern-day supermarket became commonplace, had a single player impacted the grocery industry across the entire nation. The Food Institute has been following these types of trends and reporting on them to the entire found industry since its founding back in 1928.

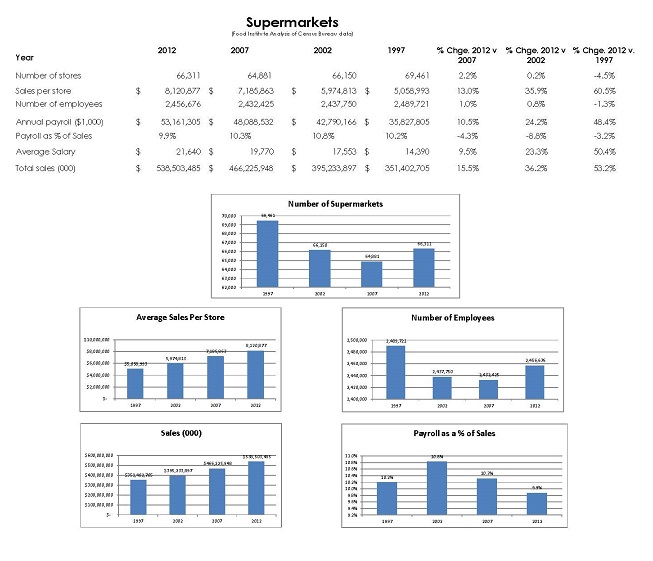

The emergence of Walmart most certainly resulted in a thinning of the supermarket ranks as some supermarkets found it impossible to compete on price with the discount retailer as it saw significant potential growth in the food sector. And of course certain market areas were affected more than others as Walmart’s impact was felt more in rural and suburban markets rather than big cities. This is borne out looking at the government’s five-year Economic Census data for retailing, for which The Food Institute found that the number of supermarkets declined by 4,580, or seven percent in the decade between 1997 and 2007. That’s only a bit less than the 4,975 stores Walmart alone operated in 2013.

Today, Walmart still leads the nation in grocery sales, holding shares over 15 percent in 75 markets major markets, according to a Morgan Stanley report on the industry. Certainly, the recession helped fuel that growth as consumers became more budget-conscious and took advantage of the availability of lower-priced food products to help manage their finances.

But supermarkets chains and independent supermarket operators have stood their ground in many cases and found ways to compete with the retail giant. From touting their more personalized service and ties to the community to investing in their own stores with new technology and amenities to keep old customers and attract new ones. More recently, the “local” movement has also made community supermarkets more attractive as well. Many operators also made sure shoppers knew they were not a cookie cutter format and strove to appeal to their local consumer base.

But supermarkets chains and independent supermarket operators have stood their ground in many cases and found ways to compete with the retail giant. From touting their more personalized service and ties to the community to investing in their own stores with new technology and amenities to keep old customers and attract new ones. More recently, the “local” movement has also made community supermarkets more attractive as well. Many operators also made sure shoppers knew they were not a cookie cutter format and strove to appeal to their local consumer base.

And it has been effective: in the five years ended in 2012, supermarket numbers rebounded, as the industry added 1,430 stores, a 2.2 percent increase. That tally was also slightly higher, by 161 units, than the 2002 store count. So, the supermarket industry is again growing.

And although the number of supermarkets dipped during the 15-year period, sales increased steadily, rising by $187 billion, to $538.5 billion in 2012, 16 percent more than in 2007, or an average 3.2 percent annually. Sales per store, meanwhile, increased by 13 percent, or an average 2.6 percent annually to $8.1 million. That compares to the average food-at-home (retail) inflation rate of 2.7 percent annually during the same period meaning those stores were not quite keeping up with the inflation rate as competition for consumers increased even well beyond Walmart to drug stores, dollar stores, warehouse clubs and more recently, online. More on that later.

The impact of the recent recession on the industry workforce can be seen as well in the Census data along with the rebound. In 2007, supermarkets employed some 2.43 million workers — two percent fewer than a decade earlier as a result, no doubt, of the lower store count. Since then, supermarkets added over 24,000 workers for a total of 2.46 million, the highest number since 1997’s 2.49 million person workforce.

One of the ways supermarkets have been competing is by watching their labor costs. Back in 2002, labor costs were the equivalent of nearly 11 percent of their sales. By 2012, that number dropped to under 10 percent. The average salary (all classes of workers), meanwhile, increased 15.5 percent in the five years ended in 2012 to $21,640 – 36.2 percent more than 2002 and 53.2 percent more than 1997.

One of the ways supermarkets have been competing is by watching their labor costs. Back in 2002, labor costs were the equivalent of nearly 11 percent of their sales. By 2012, that number dropped to under 10 percent. The average salary (all classes of workers), meanwhile, increased 15.5 percent in the five years ended in 2012 to $21,640 – 36.2 percent more than 2002 and 53.2 percent more than 1997.

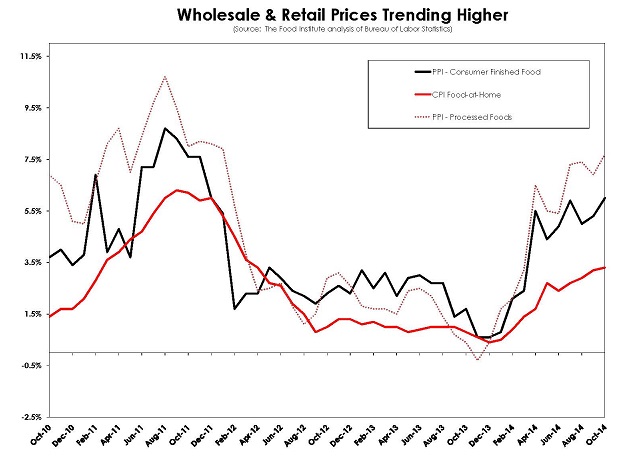

It should be noted that while grocers looked to stand out, pricing was still a primary concern to shoppers and grocers knew they still had to be competitive. And in tough economic times that means working on very slim margins. For example, for most of the recent past few years, retailers have been absorbing a greater share of the uptick in food prices. This is shown in the Producer Price Index which reflects wholesale food prices and the Consumer Price Index numbers, reflecting retail food prices.

Wholesale food prices have been advancing at a more rapid pace than retail as supermarkets have basically been protecting their budget-conscious customers by not passing on all of the price increases they encounter. This of course meant tightening the margins in an already low-margin business and cutting costs in other areas to counter that. This includes making sure all the store lights are shut off when they are not needed, according to one executive. But as noted previously, the increase in sales at supermarkets on average, has not been keeping pace with the inflation rate, so it has been a tough fight.

Looking ahead, remember that Walmart is not the only competition grocers in the U.S. are facing as more and more food products are being sold through what we call alternative channels. Warehouse clubs, drug stores and now dollar stores are selling more and more food products as their locations are well placed to attract consumers. The Food Institute estimates nearly half of warehouse club store sales come from food products, and eight to 10 percent of drug store sales. For the latter, that puts drug store food sales in excess of $15 billion annually.

Supermarkets, on the other hand, sell about $550 billion in food products each year. And while $15 billion is only about three percent of that amount, for the low-margin food business that can have a considerable impact, or $288 million weekly or over $4,000 a week for each of the over 66,000 supermarkets in the U.S. according to the latest government numbers.

So what does the future hold for supermarkets? Basically, their future promises they will be dealing with more budget-conscious consumers than in the past and a continued evolution of the food retailing industry. Online shopping continues to grow and is estimated to account for about 17 percent of retail food sales in the next decade. But supermarkets are not idly standing by and are going to have a piece of that pie as their business evolves and more of their customers go online for at least some of their grocery needs. And they will be on the lookout for ways to make their business appealing to their customer base, in the store as well as online.

About the Author